23 March 2026

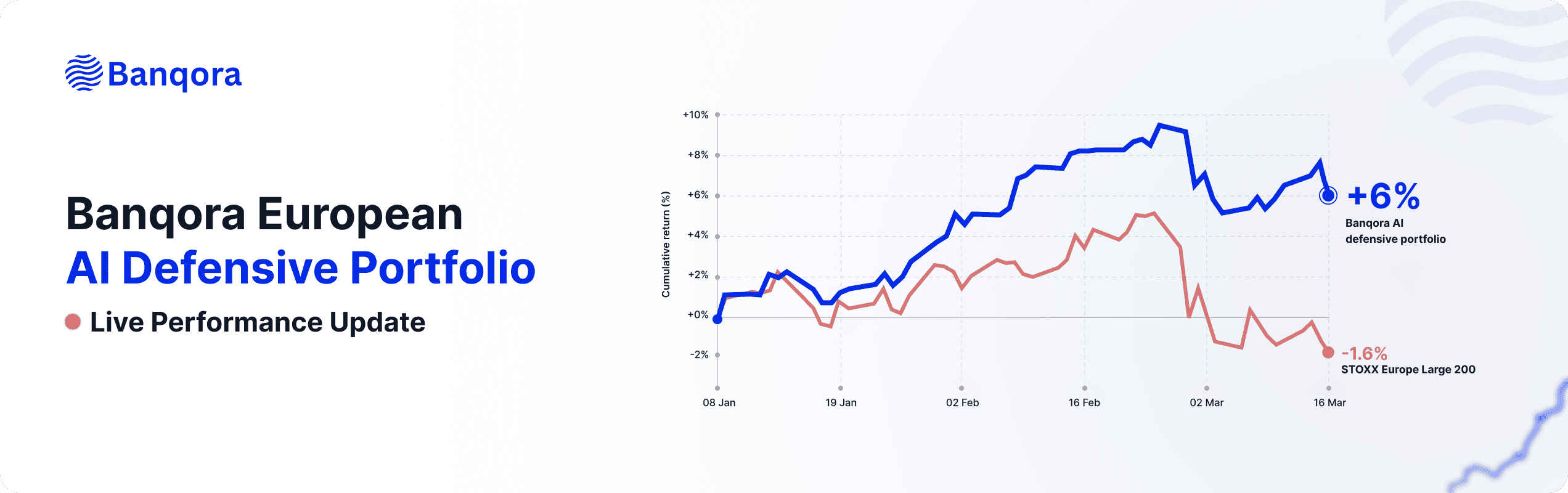

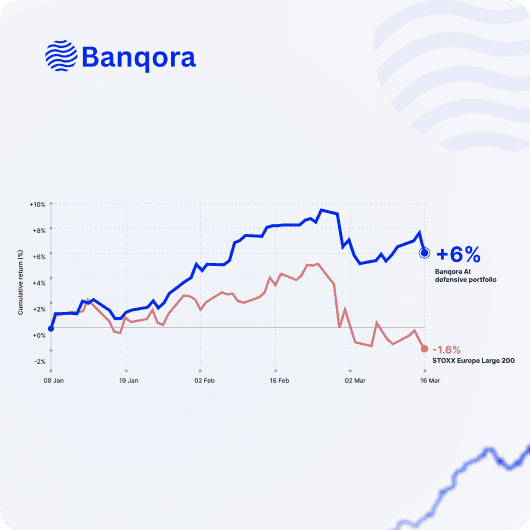

AI Defensive Portfolio: Live Performance Update

by Nicholas Holden

In January we published our AI-constructed defensive European equity portfolio, designed to minimise losses under a dotcom-style crash scenario. Ten weeks later, markets have given us a real-world test.

European equities sold off sharply through late February and March 2026, with the STOXX Europe Large 200 declining -0.8% since publication. Tariff escalation, softening macro data, and a rotation out of momentum names - exactly the conditions our agentic portfolio manager was built for.

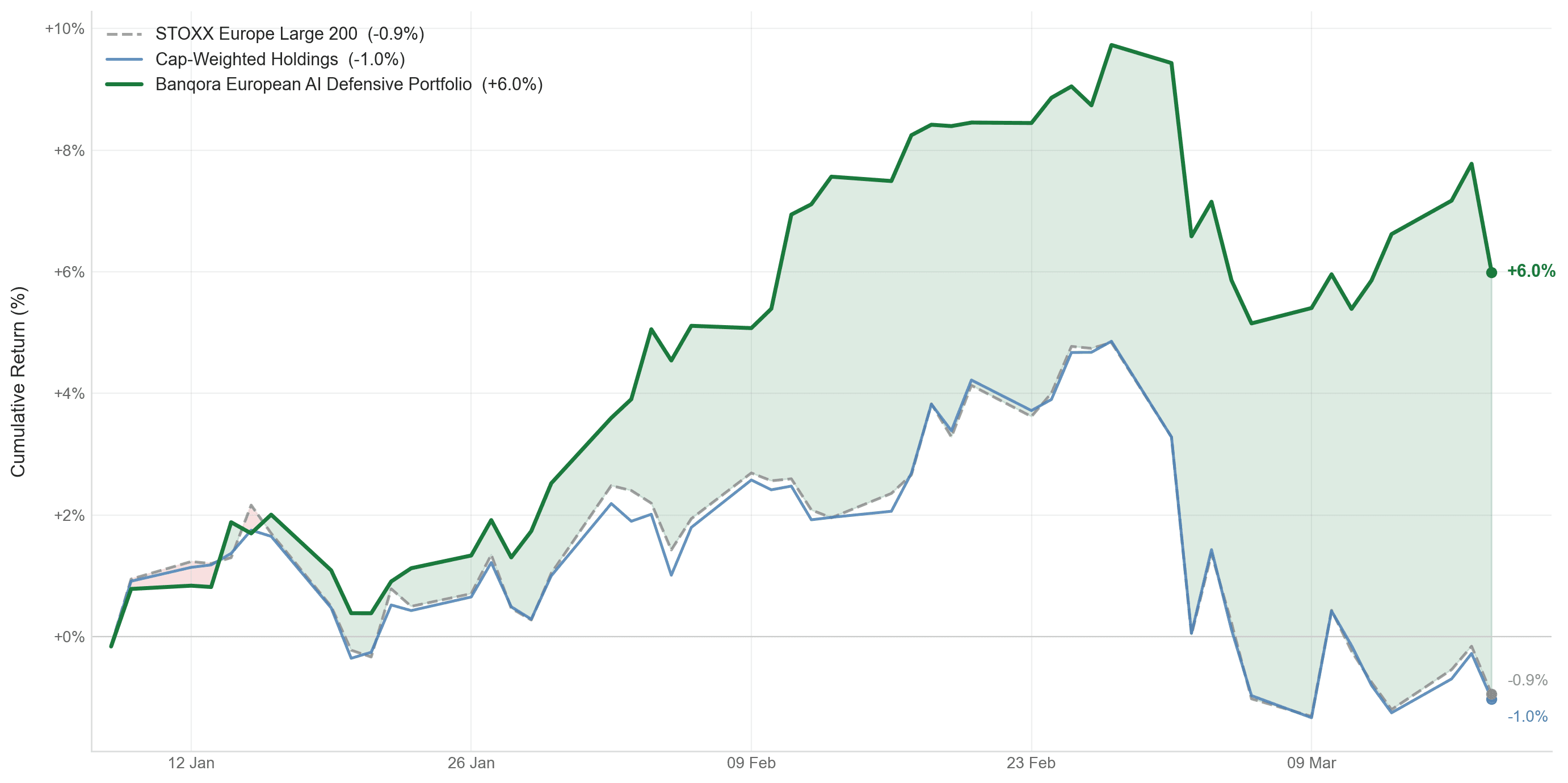

Live Results (8 Jan - 18 Mar 2026)

STOXX Europe Large 200 (Benchmark): -0.8%

Cap-Weighted Holdings: -1.1%

AI Defensive Portfolio: +6.1%

Excess Return: +6.9%

The AI defensive portfolio delivered strong positive returns through a drawdown that took the benchmark down over 6% peak-to-trough.

What Drove the Outperformance?

The agent's allocation decisions are visible in the sector attribution:

Energy (+5.6% contribution): The largest single driver from just 13% of the portfolio. TotalEnergies (+41%), Shell (+35%), Equinor (+56%), and Repsol (+54%) all rallied significantly as energy prices firmed and investors rotated into value.

Utilities (+2.2%): Defensive positioning in Engie, RWE, Iberdrola, and National Grid provided steady positive carry.

Consumer Defensive (+0.9%): Ahold Delhaize (+24%), Tesco (+15%), and Nestlé (+5%) held up as expected.

Healthcare (-1.8%): The portfolio's largest weight at 40%. Novo Nordisk (-35%) was the single biggest detractor, but the agent limited it to a 2.9% allocation - well below its benchmark weight. Diversification across Novartis (+8%), GSK (+4%), and AstraZeneca (+1%) partially offset the damage.

The cap-weighted holdings tracked the benchmark almost exactly at -1.1%, confirming that the outperformance came from the agent's active allocation decisions rather than market exposure.

Research Tools vs Portfolio Management

There's growing interest in using AI for investment management, and for good reason. LLM-powered workflows for screening names, pulling filings, and formatting research memos are genuinely useful - they compress hours of work into minutes.

But there's a meaningful gap between AI-assisted research and AI-managed portfolios. Generating a stock list is the beginning of the process, not the end. Portfolio management starts where research stops: position sizing within concentration limits, stress testing allocations against historical drawdown scenarios, enforcing liquidity and factor exposure constraints, and validating that the final portfolio holds together under adverse conditions.

Our approach embeds the AI agent within a systematic quantitative framework. The agent doesn't just pick names - it reasons through portfolio construction within the same infrastructure a professional fund would use. Every allocation is validated against drawdown limits, sector constraints, and risk budgets before it reaches the portfolio.

The +6.9% excess return over ten weeks was driven by an agent that sized positions within defined constraints, backed by industry standard infrastructure.

What This Shows

This wasn't a backtest. The portfolio was constructed and published on 8 January 2026, before the selloff began. The agent's reasoning - overweight energy and utilities, underweight momentum and rate-sensitive growth - proved directionally correct when conditions deteriorated.

More importantly, the portfolio didn't just avoid losses. It generated +6.1% absolute returns during a period where the broad market fell. That's the difference between AI that informs investment decisions and AI that executes them within a rigorous framework.